Methods of Price Determination

| Price determination is very difficult and challenging task. So, reasonable price should be determined only after identifying the factors affecting it and objectives. According to traditional practice, price can be determined through interaction between seller and buyer. But in the modern marketing, many methods of price determination have developed. The main methods are follows: |

1. Cost-oriented pricing

This cost oriented method gives special care to cost of products. The cost oriented pricing method is also divided in three classes:

a) Cost – plus pricing

This cost – plus pricing method is also called mark-up pricing. This pricing method is very simple and popular. According to this method, price of any product is determined by adding certain percent of profit. Mostly small producers and retailers use this method. Besides, construction company, legal advisors, accounting experts and other professionals determine price of products or services using this method. According to this method, special qualification or experience is not needed to fix price. So, this method can be used by any person. One imaginary example can be presented for making it clearer.

| If a pair of football shoes costs the seller Rs. 100, and the seller wants a mark-up of 25 percent, the price will be set as following: Cost-plus price = Cost + (Cost x desired mark up) Selling price = Cost + (Cost x desired mark up) = 100 + (100 x 25% = 100 + 25 Cost-plus price = Rs. 125 For making clear the cost - plus price of any goods or services, easier method can also be applied. Suppose, an umbrella has cost Rs. 200/-, if the producer wants to sell it taking 25% profit, the price of the umbrella can be determined in the following method, Cost-plus price = Unit cost + Profit margin = 200 + (25 x 2) = 200 + 50 Cost-plus price = Rs. 250 |

b) Target return pricing

Every investor invests his capital to get return. The income expected from such investment is called target result. According to target result pricing method, expected result is added to total cost and is divided by sales units. Break-even analysis can also be used for this. Such pricing policy is applied by market monopoly companies or the people’s utility organizations with mass production. Target result pricing method can be understood from the following example:

| Suppose, a pocket calculator manufacturer has the following information. Determine the price of calculator on the basis of target return. Pricing Method: Total investment = $900,000 Target return on investment = 20% Total cost = $500,000 Unit Sales = $10,000 ROI = 20/100 x 900,000 = $180,000 Per unit price = Total Cost + Target ROI/Unit Sales = 500,000 + 180,000/10,000 = 680,000/10,000 = $68 Price = $68 The unit price would be set $68. |

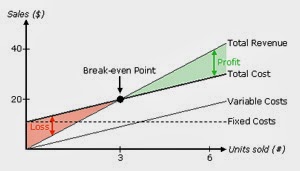

c. Break-even pricing

The situation when income and total costs become equal is called breakeven pricing. This is another important method used to determine price of products or services. In this analysis, relation between cost, quantity and profit is studied. In this breakeven situation, the firm neither earns profits nor suffers loss. If goods are produced in large quantity from breakeven point, the firm can earn more profit, but gets loss from breakeven point, the firm can earn more profit, but gets loss from the production if less quantity is produced from this point. For analyzing breakeven point, cost can be divided into two classes as (a) fixed and (b) variable. Variable cost changes with production.

If production quantity is increased, variable cost increases, and if decreased, it also decreases. Direct materials, wages and other expenses are variable costs. Fixed cost remains same even if production increases or decreases to certain limit. This means it does not increase or decrease with production quantity. Rent, interest, salary etc. are fixed costs. It is believed that while calculating breakeven point, total fixed cost and variable cost remain same per unit. To make the method of determining breakeven price clear, the following example is presented:

| Suppose a manuafacturer had the following information about a pair of shoes: Fixed costs = $32,000 Selling prie per unit = $22 Variable cost per unit = $12 Breakeven point = ? Breakeven point can be calculated using the following formula: Breakeven point (Units) = Fixed cost/Price - Variable cost = 32,000/22 - 12 = 3200 units Breakeven point (Dollar) = Fixed cost/1 - Variable cost per unit/Selling Price per unit = 32000/1 - 12/22 = 70,400 BEP ($) = 70,400

where, BEP = Break Even Point |

In the above given figure, total revenue and total cost are crossed by each other. Breakeven point is located at the cross-point. At this point, the total income can recover total cost. So, at this point of production, firm can neither earn profit nor incur loss. If the firm produces more than breakeven point, it can earn profit, otherwise it incurs losses. If the sale price is increased, BEP (Breakeven point) and market demand also decrease. This method helps to recover production cost through selling at certain price. However, fixed cost does not remain always fixed and cost cannot be classified in fixed and variable. So, it does not become useful in practice.

2. Demand oriented pricing

Demand oriented pricing method is also called profitable pricing. This method gives emphasis only on customers’ value, perception rather than to the cost of production or services and market fees. Under demand oriented pricing, the following methods can be included:

a) Perceived value pricing

This method has become very popular in determining consumer goods. According to this method, business firm collects information about consumers’ views, perception, experiences, feelings etc. Then price is determined by calculating average on the basis of such information. In this method of pricing, the cost of production is not taken as an important element/factor. The price determiner of the cost oriented products, at first determines production cost or services. But in this method, at first, customers’ perceptions are collected and average is made out from them.

b) Customer value pricing

According to the customer value pricing method, business company fixes very low price for high quality products. The company does so in order to occupy/control market share. Sometimes the market price becomes lower than cost price. This method of pricing is used by the companies having several product lines or products. Even such companies may apply this method only to some products but not to all products. They sell other products or services at premium prices. Their main purpose of doing so is to attract customers’ attention towards some products through customers’ pricing or value pricing. Such companies make a strategy to sell their other products in maximum quantity at premium price.

3. Competition Oriented Pricing

The method of determining prices of products or services by giving priority to market competition is called competition oriented pricing. This method does not care demand and production cost. In this method, price may be fixed at going on rate, more or less than market price. Under market oriented or competition oriented pricing the following methods can be used:

a) Going rate pricing

If price of products or services is determined on the basis of market price, it is called going rate. In this method, price is determined on the basis of competitors’ price (equal to the price of the products of the competing companies). This method is mostly used in fully competitive market or in same products. Generally, this method is used in steel, paper and fertilizer, agricultural and mineral products. Small companies fix price only after the big companies fix prices of their products. The companies which fix prices with this method may have their objective to face market competition.

b) Pricing below competition

The method of fixing prices lower than the competitors’ price is called pricing below competition. This method aims to attract price sensitive customers by sweeping market competitors aside. In this method, price of every product is fixed lower than the competitors’ price. This method of pricing may be very dangerous/risky, because the customers may think substitute products or service of lower quality for its lower price/rate. At such time, the related company may suffer losses.

c) Pricing above competition

According to this method, price of products or services are fixed higher than the prices fixed by competitors. Generally, such pricing method may be applied for quality products or reputed brands. This method of pricing may also be used to show to the customers that the product is of higher quality and more useful than those of competitors. This method also tries to popularize the products among customers by impressing them that the products have added quality, specialty and utility.

d) Sealed bid pricing

Sealed bid pricing is also based on competition. In this method, price is determined on the basis of estimates of the price the competitors may offer. So, in this method, production cost is not considered. Price should be fixed lower than the price offered by the bidders to get success in sealed bid. If the price becomes higher than the competitors’ price, such sealed bid may be rejected. So, the price should be fixed lower in competition than the price of the competing bidders who have registered sealed bid. Only such type of sealed bid becomes acceptable.

Some offices call sealed bids as they need to perform their works following rules and regulations. If any government office has called for sealed bid, sealed bid should be submitted giving every detail of the goods and prices. For submitting sealed bid to any office, price of products or services should be fixed. Therefore, according to this method, price should be estimated less than the price offered by competitors, but such estimate should be rational / reasonable. In government and semi-government offices in our country, if any goods or services of more than prescribed amount are to be purchased, this method is compulsorily used.

No comments:

Post a Comment